Business Income Tax Malaysia 2020

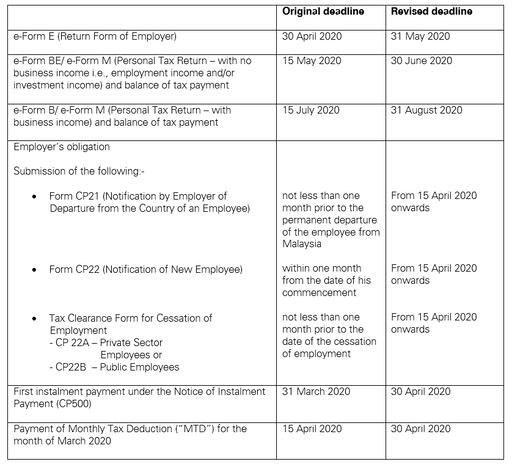

For the be form resident individuals who do not carry on business the deadline for filing income tax in malaysia is 30 april 2020 for manual filing and 15 may 2020 via e filing.

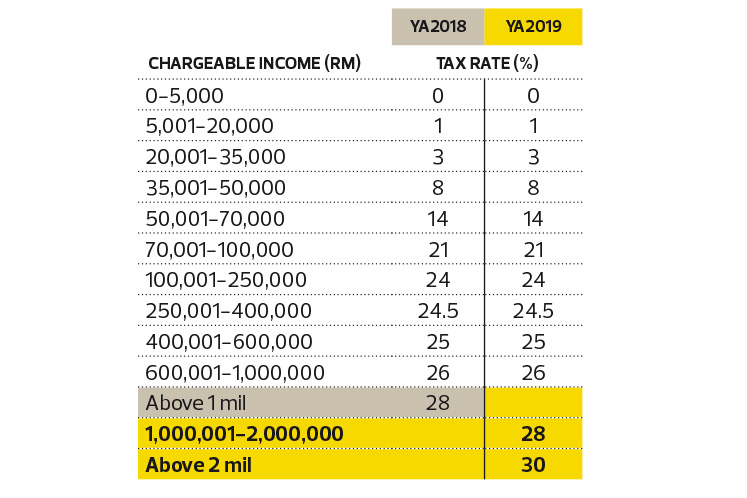

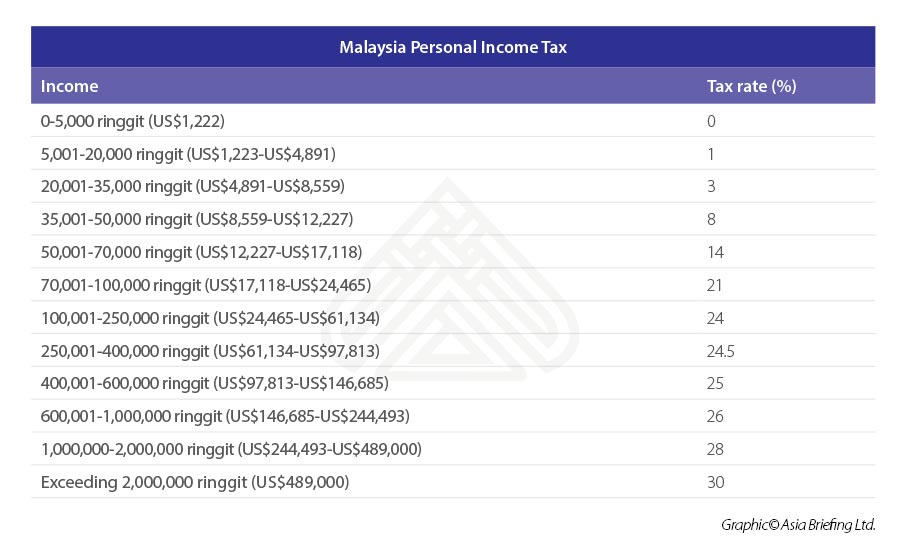

Business income tax malaysia 2020. The tax rate for 2019 2020 sits between 0 30. Rate the first rm600 000. Amending the income tax return form.

On the first 5 000. Income derived from sources outside malaysia and remitted by a resident company is exempted from tax except in the case of the banking and insurance business and sea and air transport undertakings. For non residents in malaysia the income tax rate ranges from 10 28 for ya 2019.

Thus the new deadline for filing your income tax returns in malaysia via e filing is 30 june 2020 for resident individuals who do not carry on a business and 30 august 2020 for resident individuals who carry on a business. This booklet also incorporates in coloured italics the 2020 malaysian budget proposals announced on 11 october 2019 and the finance bill 2019. With paid up capital of 2 5 million malaysian ringgit myr or less and gross income from business of not more than myr 50 million.

In budget 2020 it is proposed that the first chargeable income which is subject to the concessionary income tax rate of 17 be increased from rm500 000 to rm600 000. Headquarters of inland revenue board of malaysia menara hasil persiaran rimba permai cyber 8 63000 cyberjaya. The rate of tax for resident individuals for the assessment year 2020 are as follows.

2019 2020 malaysian tax booklet this publication is a quick reference guide outlining malaysian tax information which is based on taxation laws and current practices. You can see the full amended schedule for income tax returns filing on the lhdn website. Calculations rm rate tax rm 0 5 000.

An effective petroleum income tax rate of 25 applies on. It should be highlighted that based on the lhdn s website for the assessment year 2020 the max tax rate stands at 30. Resident companies are taxed at the rate of 24 while those with paid up capital of rm2 5 million or less and with annual sales of not more than rm50 million w e f.